RMC 49-2022: Amendment of Q and A in RMC 24-2022 (Numbers 10, 17, 31 and 33)

Aligning provisions of RMC 24-2022 with the provisions of CREATE Act

Bureau of Internal Revenue (BIR) issued Revenue Memorandum Circular (RMC) No. 49-2022 was issued on April 19, 2022 amending RMC No. 24-2022 to align the provisions with the CREATE Act and its Implementing Rules and Regulations (IRR).

I. Deferment of RR No. 09-2021 (Answer in #10) Vat Zero-Rate Remains due to Non-retroactivities rule

The deferment of RR No. 09-2021 does not only affect registered business enterprises (RBEs), thus, the provisions of RMC 24-2022 were amended through RMC 49-2022 to include other taxpayers. The RMC also reiterated that sales that have been declared by the sellers as VAT zero-rated for the period of July 01, 2021 to December 09, 2021 or a day prior to the effectivity of RR No. 21-2021 shall remain as VAT zero-rated per the non-retroactivity rule under Section 246 of the Tax Code.

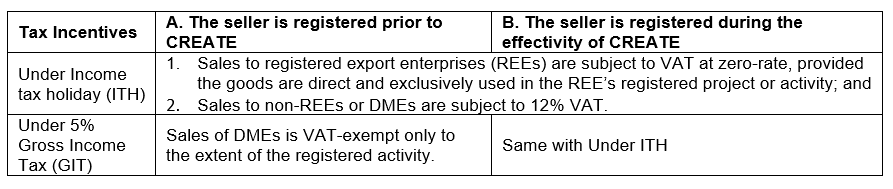

II. Following rules shall apply to the DME’s sale of goods and services: (Answer in #17) Vatability in Zero-rating status of Domestic Market Enterprises

Through the amendment of RMC 24-2022, it was also clarified that domestic market enterprises (DMEs) VAT zero-rating entitlement differs if they are registered prior to or during the effectivity of CREATE.

III. Change of status of Registered Export Enterprises (Answer in #31) REEs shifting from VAT zero-rate to VAT exempt after ITH expiration

REEs that shifted from ITH to 5% GIT or SCIT regime due to ITH expiration or who were in the 5% GIT regime at the time the CREATE Act took effect must change their registration status to non-VAT within two (2) months. On the other hand, a taxpayer who has other activities that are subject to VAT other than those registered with the IPA shall remain a VAT taxpayer and shall report the sales in the VAT returns as VATable, zero-rated, and/or VAT-exempt.

IV. Condition for sales to be accorded as VAT zero-rating (Answer in #33) Local Suppliers Transition to VAT zero-rating status/ accreditation to exempt within 3 months from RMC 24-2022 effectivity

Prior approval from the BIR is still required for local suppliers of goods/services to registered export enterprises to receive VAT zero-rating on their sales. However, if a transaction qualifies for VAT zero-rating but fails to secure an approved application with the BIR, prior approval may not be required until March 09, 2022 or before the issuance of RMC 24-2022, and will only be subject to the three (3) following documentary requirements:

- Certificate of Registration and VAT Certification issued by the concerned IPA;

- Sworn Declaration – stating that the goods/services being purchased shall be used directly and exclusively in the registered project; and

- Other documents to corroborate entitlement to VAT zero-rating.

For everyone’s guidance and perusal.

DISCLAIMER: The advisory is not a substitute for an expert opinion and is purely a general research that may have not considered the entirety of other related topics. Any tax and/or compliance advice is not intended or written by the author to be used, and cannot be used, by a client or any other person or entity for the purpose of (i) avoiding penalties that may be imposed on by the regulatory bodies, or (ii) promoting, marketing, or recommending to another party any matters addressed herein.

The opinion or advice expressed in this advisory is based on the facts and circumstances gathered. Any inaccuracy in any of the assumptions set forth above may have the effect of changing all or part of this report, and this report may not apply. The advice is based on our interpretation of the provisions of the Code, the Revenue Regulations promulgated and issued by the tax bureau, BIR positions as set forth in published Revenue Rulings, other pronouncement, orders and circulars, and judicial decisions in effect on the date of this report, any of which could be changed at any time. Any such changes may be retroactive and could significantly modify the statements and opinions/ advice expressed herein In effect, this might render the advisory obsolete or incorrect in partial or in full. We undertake no obligation to advise you of changes that may hereafter be brought to our attention.

Blog Category

Related Post

- Bonusy, pokies i sloty w polskim kasynie online – Sprawdź nasze promocje!

- Odkryj Najlepsze Bonusy i Sloty w Polskim Kasynie Online

- Navigating New Horizons – Doing Business in The Philippines Guide 2025

- i-Lead Academy Manual for Members/Students

- Foreign Currency Transactions Treatment for Financial Reporting and Tax Reporting Purposes