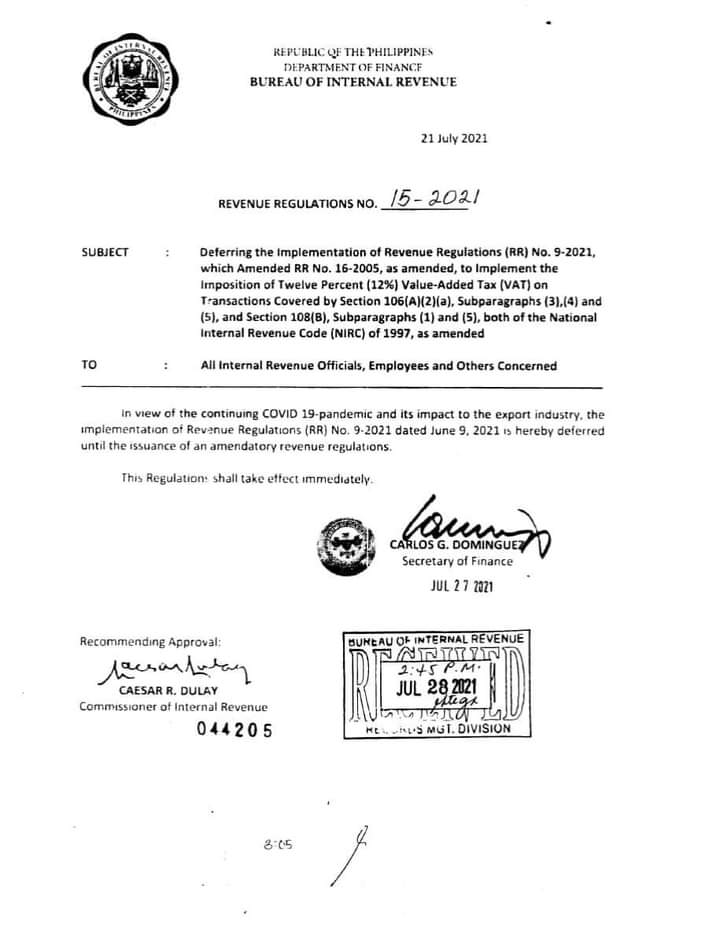

REVENUE REGULATIONS (RR) No. 15-2021

Posted by Michael Aguirre on February 19th, 2022

Deferred implementation of RR No. 9-2021 which imposed a 12% value-added tax (VAT) on specified exporter transactions that were previously subjected to 0%

The Bureau of Internal Revenue (BIR) has recently issued RR No. 15-2021 deferring the implementation of RR No. 9-2021 until the issuance of an amendatory revenue regulations.

With the deferral of RR No. 9-2021, the following transactions will revert to their zero-rated status:

- Sale of raw materials or packaging materials to a non-resident buyer for delivery to a local export-oriented enterprise;

- Sale of raw materials or packaging materials to export-oriented enterprise whose export sales exceed 70 percent of total annual production;

- Those considered export sales under Executive Order (EO) No. 226, or the Omnibus Investment Code of 1987, and other special laws (Section 106 (A) (2) (a) (5) of the Tax Code, as amended);

- Processing, manufacturing, or repacking goods for other persons doing business outside the Philippines which goods are subsequently exported; and

- Services performed by subcontractors and/or contractors in processing, converting, or manufacturing goods for an enterprise whose export sales exceed 70 percent of total annual production.

The deferment of RR 9-2021 is seen to provide a big relief for direct and indirect exporters that are already affected by the pandemic to continue their normal business operation procuring from local suppliers.

Attached also is a copy of Revenue Regulations No. 15-2021 for your reading pleasure.

Blog Category

Related Post

- Bonusy, pokies i sloty w polskim kasynie online – Sprawdź nasze promocje!

- Odkryj Najlepsze Bonusy i Sloty w Polskim Kasynie Online

- Navigating New Horizons – Doing Business in The Philippines Guide 2025

- i-Lead Academy Manual for Members/Students

- Foreign Currency Transactions Treatment for Financial Reporting and Tax Reporting Purposes